Examples¶

RlassoModels includes four estimators Rlasso, RlassoLogit, RlassoPDS and RlassoIV. The dataset from Acemoglu, Johnson and Robinson (2001) will be used as a running example, to highlight the different models. This is dataset is also used for various examples in the stata packages lassopack and pdslasso by Ahrens, Hansen & Schaffer (2018, 2020) on which

RlassoModels is largely based. See also the R version HDM (Chernozkukov, Hansen & Spindler, 2016).

[1]:

# imports

from rlassomodels import Rlasso, RlassoPDS, RlassoIV

from sklearn.linear_model import LassoCV, LassoLarsIC, LassoLarsCV

from collections import defaultdict

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from numpy.testing import assert_equal

[2]:

# get data and select y and X

ajr_df = pd.read_stata("https://statalasso.github.io/dta/AJR.dta")

X = ajr_df[["lat_abst", "edes1975", "avelf", 'temp1', 'temp2', 'temp3', 'temp4', 'temp5', 'humid1',

"humid2", 'humid3', 'humid4' ,"oilres","steplow", "deslow", "stepmid","desmid", "drystep",

"drywint", "landlock", "goldm", "iron", "silv", "zinc"]]

y = ajr_df["logpgp95"]

print(f"Dimensions: {ajr_df.shape}")

ajr_df.head()

Dimensions: (64, 36)

[2]:

| shortnam | logpgp95 | avexpr | lat_abst | logem4 | edes1975 | avelf | temp1 | temp2 | temp3 | ... | zinc | oilres | baseco | _merge | indtime | euro1900 | democ1 | cons1 | democ00a | cons00a | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | AGO | 7.770645 | 5.363636 | 0.136667 | 5.634789 | 0.0 | 0.772755 | 26.0 | 28.0 | 37.0 | ... | 0.0 | 146000.0 | 1.0 | matched (3) | 20.0 | 8.000000 | 0.0 | 3.0 | 0.0 | 1.0 |

| 1 | ARG | 9.133459 | 6.386364 | 0.377778 | 4.232656 | 90.0 | 0.176932 | 17.0 | 25.0 | 40.0 | ... | 0.0 | 46900.0 | 1.0 | matched (3) | 170.0 | 60.000004 | 1.0 | 1.0 | 3.0 | 3.0 |

| 2 | AUS | 9.897972 | 9.318182 | 0.300000 | 2.145931 | 99.0 | 0.112797 | 17.0 | 18.0 | 43.0 | ... | 12.0 | 99100.0 | 1.0 | matched (3) | 94.0 | 98.000000 | 10.0 | 7.0 | 10.0 | 7.0 |

| 3 | BFA | 6.845880 | 4.454545 | 0.144444 | 5.634789 | 0.0 | 0.546718 | 29.0 | 38.0 | 48.0 | ... | 0.0 | 0.0 | 1.0 | matched (3) | 35.0 | 0.000000 | 0.0 | 3.0 | 0.0 | 1.0 |

| 4 | BGD | 6.877296 | 5.136364 | 0.266667 | 4.268438 | 0.0 | 0.000000 | 25.0 | 29.0 | 42.0 | ... | 0.0 | 0.0 | 1.0 | matched (3) | 23.0 | 0.000000 | 8.0 | 7.0 | 0.0 | 1.0 |

5 rows × 36 columns

Rlasso¶

The class Rlasso is a scikit-learn compatible estimator that implements the lasso and square-root lasso with data-driven and theoretically justified penalty level (see: Belloni et al.,2011, 2013). It adopts the syntax where all hyperparameters are definied upon class instantiation and data, or data-dependent arguments, is passed to the fit() method. This for example means that it can be passed to a

pipeline. In adition, it is also possible to call fit_formula() which uses R-style model specification, made possible by the package patsy.

[3]:

# define model and fit

rlasso = Rlasso(post=True, sqrt=False, cov_type="robust")

res1 = rlasso.fit(X,y)

# fit same model but using formula

formula = "logpgp95 ~ " + " + ".join(X.columns)

res2 = rlasso.fit_formula(formula, data=ajr_df)

assert_equal(res1.coef_, res2.coef_)

We can compare the results of different Rlasso specifications to common alternatives for choosing  , featured in

, featured in sklearn.

[4]:

# define models

models = {

"rlasso": Rlasso(post=False), # post-lasso is default

"sqrt-rlasso": Rlasso(sqrt=True, post=False),

"rlasso-post": Rlasso(),

"AIC": LassoLarsIC(criterion="aic", normalize=False),

"BIC": LassoLarsIC(criterion="bic", normalize=False),

"CV": LassoLarsCV(cv=5,normalize=False)

}

results = {}

for name, model in models.items():

tmp_res = model.fit(X,y)

results[name] = np.array([tmp_res.intercept_] + tmp_res.coef_.tolist())

pd.DataFrame(results, index=["intercept"] + X.columns.tolist()).round(3)

[4]:

| rlasso | sqrt-rlasso | rlasso-post | AIC | BIC | CV | |

|---|---|---|---|---|---|---|

| intercept | 7.981 | 7.952 | 8.141 | 7.039 | 7.039 | 7.580 |

| lat_abst | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| edes1975 | 0.011 | 0.009 | 0.018 | 0.021 | 0.021 | 0.015 |

| avelf | -0.270 | -0.137 | -1.004 | 0.000 | 0.000 | -0.450 |

| temp1 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.165 |

| temp2 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | -0.027 |

| temp3 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | -0.062 |

| temp4 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | -0.075 |

| temp5 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | -0.007 |

| humid1 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.002 |

| humid2 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.003 |

| humid3 | 0.000 | 0.000 | 0.000 | 0.012 | 0.012 | 0.023 |

| humid4 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | -0.018 |

| oilres | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| steplow | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | -0.138 |

| deslow | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| stepmid | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| desmid | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| drystep | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| drywint | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| landlock | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| goldm | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.022 |

| iron | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.004 |

| silv | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.035 |

| zinc | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

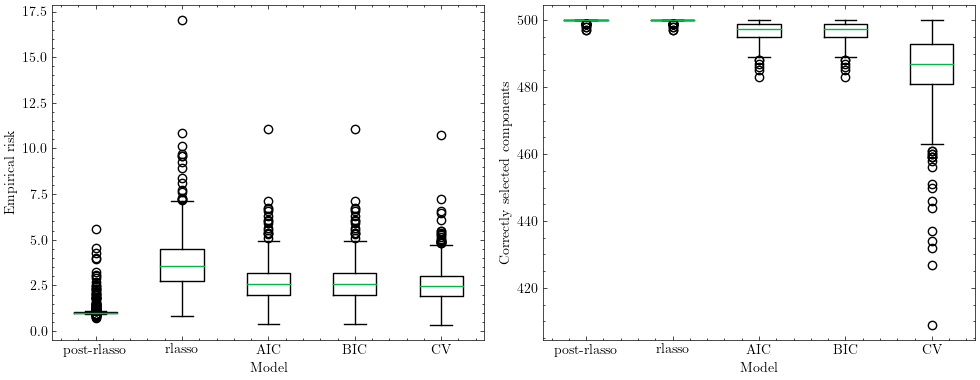

As can be seen, rlasso tends to produce sparse solutions compared to cross-validation and in this example, selecting other variables than both AIC and BIC. To get an insight into the performance of Rlasso, estimates can be compared to the oracle estimator of running OLS only on active components. As can be seen from the example below, post-rlasso, that is running OLS on the rlasso selected components, significantly outperforms all other models and achives near oracle performance. Looking at the second plot, it is easy to see that this must be the case since rlasso almost always selects all the correct components.

[5]:

def sparse_dgf():

"""

Data-generating function following Belloni (2011).

Taken from statsmodels tests:

https://github.com/statsmodels/statsmodels/blob/c1e30d9534dbe56346e50517da4dacf023a4aad7

/statsmodels/regression/tests/test_regression.py#L1311

"""

# Based on the example in the Belloni paper

n = 100

p = 500

ii = np.arange(p)

cx = 0.5 ** np.abs(np.subtract.outer(ii, ii))

cxr = np.linalg.cholesky(cx)

X = np.dot(np.random.normal(size=(n, p)), cxr.T)

b = np.zeros(p)

b[:5] = [1, 1, 1, 1, 1]

y = np.dot(X, b) + 0.5 * np.random.normal(size=n)

return X, y, b, cx

oracle_ratio = defaultdict(list)

correct_selected = defaultdict(list)

n_sims = 500

models = {

"rlasso":Rlasso(post=False),

"post-rlasso":Rlasso(),

"AIC": LassoLarsIC(normalize=False,noise_variance=0.5),# needs sigma when p>n

"BIC": LassoLarsIC(normalize=False,noise_variance=0.5),# needs sigma when p>n

"CV": LassoLarsCV(cv=5,normalize=False)

}

def oracle_sim():

for _ in range(n_sims):

X,y,b,cx = sparse_dgf()

# oracle estimator (OLS) on true support

X_oracle = X[:,:5]

oracle_est = np.zeros(X.shape[1])

oracle_est[:5] = np.linalg.solve(X_oracle.T@X_oracle, X_oracle.T@y)

oracle_e = np.zeros(X.shape[1])

oracle_e = oracle_est - b

oracle_selected = oracle_est != 0

denom = np.sqrt(np.dot(oracle_e, np.dot(cx, oracle_e)))

for name, model in models.items():

# get estimate

est = model.fit(X, y)

e = est.coef_ - b

selected = est.coef_ != 0

numer = np.sqrt(np.dot(e, np.dot(cx, e)))

# get ratio

oracle_ratio[name].append(numer / denom)

# correctly selected components

correct_selected[name].append((oracle_selected == selected).sum())

# plot results from simulations

# oracle ratio

with plt.style.context("science"):

fig, axs = plt.subplots(ncols=2, dpi=100, figsize=(10,4))

axs[0].boxplot([oracle_ratio["post-rlasso"], oracle_ratio["rlasso"],

oracle_ratio["AIC"], oracle_ratio["BIC"],

oracle_ratio["CV"]])

axs[0].set_ylabel("Empirical risk")

axs[0].set_xlabel("Model")

axs[0].set_xticks([1,2,3,4,5],["post-rlasso", "rlasso", "AIC", "BIC", "CV"])

# correctly selected components

axs[1].boxplot([correct_selected["post-rlasso"], correct_selected["rlasso"],

correct_selected["AIC"], correct_selected["BIC"],

correct_selected["CV"]])

axs[1].set_ylabel("Correctly selected components")

axs[1].set_xlabel("Model")

axs[1].set_xticks([1,2,3,4,5],["post-rlasso", "rlasso", "AIC", "BIC", "CV"])

plt.tight_layout()

plt.show()

oracle_sim()

RlassoPDS¶

RlassoPDS extends Rlasso to be used for causal inference in the following setting

Where  is a scalar exogenous variable (can also be low-dimensional vector) for which we are interested in a obtaining a consistent estimate with valid standard errors and test statistics in the presence of high-dimensional

is a scalar exogenous variable (can also be low-dimensional vector) for which we are interested in a obtaining a consistent estimate with valid standard errors and test statistics in the presence of high-dimensional  . This is possible using the post-double-selection (PDS) and post-regularization (CHS) methodology developed in a series of papers by Belloni et al. (2011, 2013, 2014) and Chernozhukov et al. (2015). By default both methods are used. Since the

purpose is inference and we’re interested in a limited amount of variables, the class is purposly no longer directly scikit-learn compatible. Instead, it uses the econometrics package linearmodels in the final estimation stage to produce relevant outputs. This is shown below by considering a case where we want to perform inference for the variable

. This is possible using the post-double-selection (PDS) and post-regularization (CHS) methodology developed in a series of papers by Belloni et al. (2011, 2013, 2014) and Chernozhukov et al. (2015). By default both methods are used. Since the

purpose is inference and we’re interested in a limited amount of variables, the class is purposly no longer directly scikit-learn compatible. Instead, it uses the econometrics package linearmodels in the final estimation stage to produce relevant outputs. This is shown below by considering a case where we want to perform inference for the variable avexpr:

[6]:

d_exog = ajr_df["avexpr"]

rlasso_pds = RlassoPDS().fit(X,y,D_exog=d_exog)

print(rlasso_pds.summary())

print(f"Std. Errors and Test statistics valid for\n{rlasso_pds.valid_vars_}")

Model Comparison

============================================

PDS CHS

--------------------------------------------

Dep. Variable logpgp95 logpgp95

Estimator OLS OLS

No. Observations 64 64

Cov. Est. unadjusted unadjusted

R-squared 0.7261 0.4199

Adj. R-squared 0.7075 0.4107

F-statistic 169.67 46.318

P-value (F-stat) 0.0000 1.005e-11

================== ============ ============

const 5.7641***

(0.3774)

avexpr 0.3913*** 0.3913***

(0.0562) (0.0575)

avelf -0.9975***

(0.2474)

edes1975 0.0091***

(0.0032)

zinc -0.0079

(0.0281)

--------------------------------------------

Std. Errors reported in parentheses

Std. Errors and Test statistics valid for

['avexpr']

RlassoIV¶

RlassoIV is used when one wants to use instruments in order to estimate low-dimensional endogenous variables in the setting

where both z_i and x_i are possibily high-dimensional. Note that we can still include exogonous variables. In the example below, we now treat avexpr as endogenous and specify that rigorous lasso should be used both to select instruments and controls.

[7]:

# get data and select y and X

ajr_df = pd.read_stata("https://statalasso.github.io/dta/AJR.dta")

# some instruments have NaN values

ajr_df.dropna(inplace=True)

X = ajr_df[["edes1975", 'temp1', 'temp2', 'temp3', 'temp4', 'temp5', 'humid1',

"humid2", 'humid3', 'humid4' ,"oilres","steplow", "deslow", "stepmid","desmid", "drystep",

"drywint", "landlock", "goldm", "iron", "silv", "zinc", "lat_abst", "avelf"]]

y = ajr_df["logpgp95"]

# subset instruments and endogenous var

Z = ajr_df[["logem4", "euro1900", "democ1", "cons1","democ00a", "cons00a"]]

d_endog = ajr_df["avexpr"]

[8]:

rlasso_iv = RlassoIV(select_X=True, select_Z=True)

rlasso_iv.fit(X, y, D_exog=None, D_endog=d_endog, Z=Z)

print(rlasso_iv.summary())

print(f"Std. errors and Test statistics valid for\n{rlasso_iv.valid_vars_}")

Model Comparison

==================================================

PDS CHS

--------------------------------------------------

Dep. Variable logpgp95 logpgp95

Estimator IV-2SLS IV-2SLS

No. Observations 59 59

Cov. Est. unadjusted unadjusted

R-squared 0.4334 -0.5831

Adj. R-squared 0.3915 -0.6104

F-statistic 66.517 7.3846

P-value (F-stat) 1.232e-13 0.0066

================== ============ ============

const 3.1400*

(1.6429)

avelf -0.7468**

(0.3605)

edes1975 0.0025

(0.0070)

zinc -0.0658

(0.0523)

avexpr 0.8034*** 0.9095***

(0.2687) (0.3347)

==================== ============== ==============

Instruments euro1900 instruments

logem4

--------------------------------------------------

Std. Errors reported in parentheses

Std. errors and Test statistics valid for

['avexpr']

References¶

Acemoglu, D., Johnson, S., & Robinson, J. A. (2001). The colonial origins of comparative development: An empirical investigation. American economic review, 91(5), 1369-1401.

Ahrens, A., Hansen, C. B., & Schaffer, M. (2020). LASSOPACK: Stata module for lasso, square-root lasso, elastic net, ridge, adaptive lasso estimation and cross-validation.

Ahrens, A., Hansen, C.B., Schaffer, M.E. 2018. pdslasso and ivlasso: Programs for post-selection and post-regularization OLS or IV estimation and inference. http://ideas.repec.org/c/boc/bocode/s458459.html

Chernozhukov, V., Hansen, C., & Spindler, M. (2016). hdm: High-dimensional metrics. arXiv preprint arXiv:1608.00354.

Chernozhukov, V., Hansen, C., & Spindler, M. (2015). Post-selection and post-regularization inference in linear models with many controls and instruments. American Economic Review, 105(5), 486-90.

Belloni, A., Chen, D., Chernozhukov, V. and Hansen, C. (2012). Sparse models and methods for optimal instruments with an application to eminent domain. Econometrica 80 (6), 2369-2429.

Belloni, A., Chernozhukov, V. and Hansen C., (2013). Inference for high-dimensional sparse econometric models. In Advances in Economics and Econometrics: 10th World Congress, Vol. 3: Econometrics, Cambridge University Press: Cambridge, 245-295.

Belloni, A., Chernozhukov, V., Hansen, C. (2014). Inference on treatment effects after selection among high-dimensional controls. The Review of Economic Studies 81(2), 608-650..